Bringing Sexy Back to a Stock

Along with Market Worries and a Good Way to Burn 120 Hours

First month down, thanks for reading!

Important Items of Last Week

Thoughts on the market

I grow more wary. We’ve had a nice run. The bullish side seems overly represented in positioning now. I own a few hundred bps of S&P puts, generally with Sept expy.

“From October 2022 to July 2023, the S&P 500’s forward PE multiple rose 30%, while the Technology sector’s forward PE surged 52%. The Technology PE is particularly eye popping, having reached 28x forward in late July, which brought it back to its 2021 peak, an incredibly different interest rate and monetary policy environment. In late 2021, real interest rates were an ultra-accommodative -1.2% compared to today’s +1.7% for the 10 year. In the past, tech valuations and real interest rates have been closely related, however this relationship broke down completely in 1H23. Even the broad S&P 500 reached fairly rarified air from a valuation perspective in late July, touching 20x forward earnings, a level that has only been eclipsed two other times in the past 30 years: the 1990’s tech bubble and the 2020-2021 COVID policy-fueled bubble.” -Cameron Dawson, NewEdge Wealth [Via

]While journalists and talking heads speak about inflation being tamed, energy prices are climbing back from the lows. Diesel and natural gas prices are up 40-50% in four months. Gasoline futures are at the highest levels since Oct 2022. We are still YoY comping below but if these dynamics hold energy won’t continue to be deflationary.

Everyone getting back in the pool. CTA’s are at the highest % equity ownership in the last year (via

]. The Fed may pause, thereby exciting Bulls (though pausing and cuts have generally presaged previous market selloffs). Meanwhile, over the last year, everyone became a put seller because the market kept going up and Vol collapsed. This regime could get messy if we get something more than the down 1% days people now treat as drawdowns.

As

has outlined quite well, there is a likely probability that longer-dated treasury rates continue to be under pressure. This puts pressure on equity multiples and numerous pressure points of the economy.It seems likely we’ll start to see unemployment tick up. ZipRecruiter collapsed as employers post fewer jobs and spend less to advertise, braking previous seasonal patterns. From ZIP’s POV at least, recruiting budgets have been slashed at both the SMB and enterprise level.

Everyone hates China. WSJ. Bloomberg. The Guardian. Even Biden got in on the bashing, in a bit of pot/kettle, calling the Chinese economy a ‘ticking time bomb.’ China has many medium-to-longer-term issues, but has levers it can pull to stimulate its consumer. Like most collective groups, the CCP enjoys having power. The key to that is to keep the economy humming. I find it hard to believe they don’t try stimulating their way out of being the next Japan. That makes select Chinese equities buy and rents. I’m long some BABA.

Heard from my friends

Despite the need to deploy loans at higher rates to offset their higher cost of deposits, Banks aren’t lending on real estate projects. The locals and regionals won’t even touch class A in growing cities on projects backed by well-capitalized investors. The banks’s lending abilities are bound because they are over-indexed to RE sector and due to other general balance sheet issues. The economy isn’t grinding to a halt because non-bank lenders stepped in to provide capital.

From my POV, this is a negative for the small/regional banks as it prevents them from profiting from higher rates while their costs elevate. While the sector had a nice run, I suspect the regionals come under pressure again. Costs are higher, profits aren’t growing as would be expected from higher rates, and the continued rise in long-dated Treasury rates will put more pressure on held-to-maturity securities. Thus we could see another swoon in this sector which has been a recent strong performer. I’m short a bit of KRE.

Things that WERE NOT important… but I enjoyed

The American Dream is Still Alive

He’s Heard About Pod Signing Bonuses

US Rowing’s Transgender Policy is Amazing

Of all the various athletic league responses to transgendered athletes, US Rowing’s is the most astounding in its seeming indifference to females but protection of male sport sanctity.

Per US Rowing, in all non-elite or NCAA events, one can row in whatever gender category one feels like. There is one significant exception… you have to row with your birth sex in co-ed boats. So my friend who is a 6’6 former jr Olympian could decide he feels female and row solo or with an all-female crew in an amateur event. Despite being 20 years past his prime I would heavily bet on his chances in that race. However… he couldn’t join a mixed-gender crew because that would affect the sport for other men.

USRowing, recognized by the U.S. Olympic and Paralympic Committee as the sport’s national governing body, issued an updated gender-identity policy in December of last year.

The new policy, to be revised annually, permits rowers to declare confidentially that they are women, without any medical treatment or documentation, and race in women’s categories in regattas that are not run by World Rowing (the international rowing federation formerly known as FISA), or under the jurisdiction of the NCAA or “other national rowing governing organizations.” Mixed events are the only ones in which the new USRowing policy addresses “athletes assigned as female at birth.”

“This policy destroys fair competition for girls and women, but it protects it for boys and men. By allowing males to identify as girls and women to compete in the women’s category, fairness for female athletes is blatantly discarded,” said Dr. Mary O’Connor, an Olympic rower and a member of the Independent Council on Women’s Sports (ICONS).

“USRowing made sure that fairness and competition was protected for boys and men by defining eligibility based on sex in only one category—the mixed-boats category,” said O’Connor, who was among the Yale women who stripped naked and wrote “Title IX” on their bodies in 1976 to advance women’s sports.

“Why? Because if they did not do so, that would make competition unfair for men potentially if the men were competing in a mixed event against boats with males who identified as women.

“This is the only category—namely, when females are racing with men—in which being female is the criterion for inclusion. Otherwise, women have to compete in women’s events against men who identify as women.

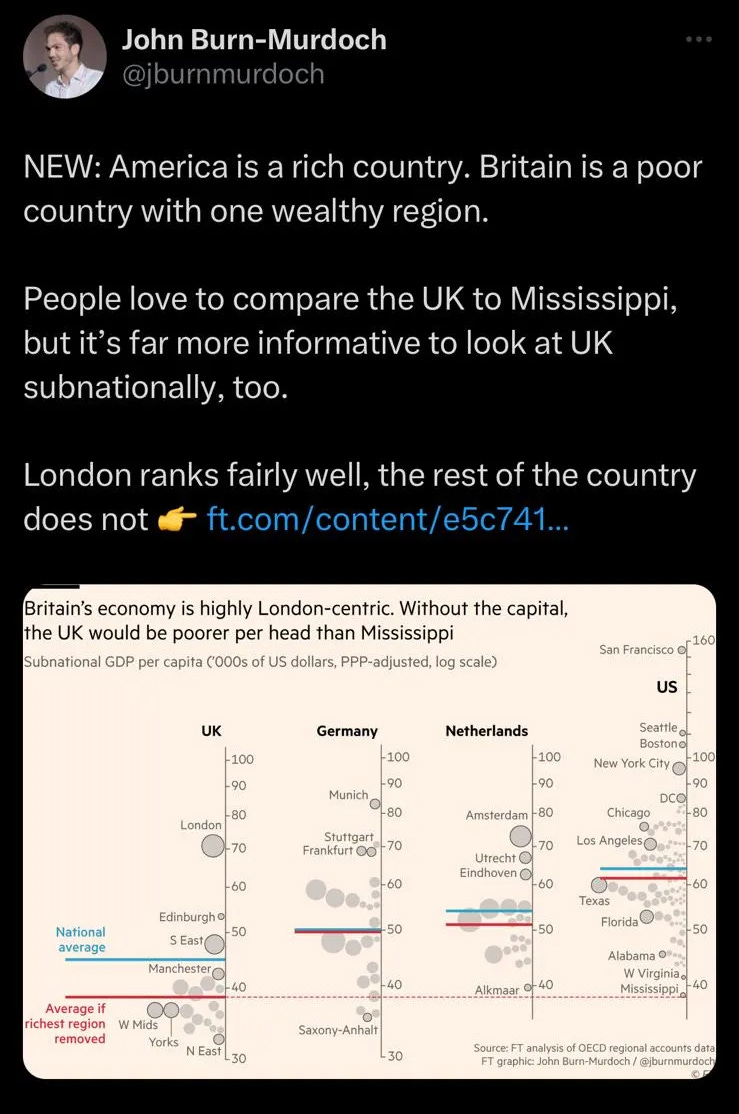

I Better Understand Pro-Brexit Ferver Now

I had no idea that this is how the UK sans London looks on GDP/Capita. Even Edinburgh is quite low vs where any tier 1 US city would be.

Money Stuff: Director’s Cut

Good grab from the NY Mag D-Sol takedown by the GOAT, Matt Levine. If you don’t subscribe to Money Stuff, you’re doing life wrong.

Market Wizards III: Portnoy Edition

Portnoy has a spot next to Kris Jenner and Steve Jobs in my marketing hall of fame. He buil a Boston area fantasy sports advice publication into a national brand through a pizza review blog and frat sports humor. Then he took some money off the table through a PE partnership, cashed out by selling to Penn Gaming, then bought all the equity (and cash flows) back for the cost of schmuck insurance because Barstool company was never actually a great fit for PENN and he recognized he had leverage on PENN due to its desire to partner with DIS/ESPN. He ran an absolute master class of business.

Stocks I Don’t Want to Own

Always love these pitches on VIC. Small-cap Bulgarian company listed in Germany where either the price will be manipulated or it will be left for dead?? Yes!

Stock idea of the week

Update on several names - Not something I always plan on doing, but literally every name I’ve written about had a recent update.

CUTR

Messy, messy quarter. The new CEO has his hands full righting the ship. This will include stabilizing the legacy business and improving the business model around AviCure. The volatility in names like CUTR is extreme, but AviCure and Taylor will lead the way to positive volatility that, inshallah, will yield multi-bag return from here. This is a 2% for me as I added to a small position after the report; I’ll look to size it back up after they set forth their new plan for improving utilization and righting the legacy business. There will still be plenty of meat on the bone then.

ATVI

The CMA has taken longer to give a preliminary opinion than they forcasted, causing ATVI to drift a little lower. Despite the stock bleeding off a little, I see the delay as a combination of August-in-Europe and a positive indication. My reason for optimism: We are in the middle of the CMA stumbling through a DIY process in response to pressure from politicians, the CTA, and consumers. A hard no is easy for the CMA as it wraps up this ad hoc process. Meanwhile, altering the decision to a yes to MSFT/ATVI is a new precedent that includes the need to do additional steps. The CMA wants to avoid carving paths they don’t want available to other companies. I reduced this position by 15% early last week for margin reasons and with the stock at 91 I have re-added a lot of that exposure.

SSTI

Strong revenue growth and customer wins, they admited Chicago’s contract renewal looking better, terrible OpEx. Fortunately, most of the latter is one time. You don’t own SSTI for its earnings. You own it for them expanding miles under management, which will continue. When, inshallah, Chicago renews the contract SSTI will be up 50%+ from here. I added on the stock fall on the report, which was nice given the fast recovery (have to love small cap vol). This is now a 4%. It would be larger if I wasn’t tepid on my market view over the next two months.

New Idea: GPN.

Former market darlings where investors moved on due to concerns can create great investment opportunities. This happened to MSFT in the early 2010’s. Then ValueAct got involved, Satya came in, and it appreciated 10x over the next decade. I do not expect the same appreciation in GPN, but it could be a great compounder over the next several years.

Global Payments provides merchant acquiring services (the ability to process credit card payments) for retailers and other places people pay with card. This is 70% of revs and 80% of profit and GPN generates revenue mostly through taking a tiny piece of transaction volume along with fees for value added services they provide to customers. Most of the remaining business is software and services that help financial institutions to oversee their card networks; this revenue is generated through the number of transactions on issued bank cards. Generally, revenues grow by GPN taking share - from GPN winning new customers, from GPN purchasing smaller companies - and through an increase in credit card transaction volume. The latter usually follows Visa / Mastercard growth as credit cards take share and general merchant spend velocity.

GPN has historically been a strong performer - it appreciated 500% in the past decade - but the post-COVID period has been weak for the stock due to market psychology and fundamental reasons. Enthusiasm for GPN, and most legacy payment players from FLT to FISV, waned as investors worried merchant acquirers could not compete with TOST and various VC backed companies and that Buy-Now-Pay-Later would take a meaningful bite out of the the credit card payment pie. As a validation to this worry, organic sales for GPN slowed as they digested the Total System Service merger of equals that had the bad fortunate to close at the beginning of COVID. Then spinoffs in 2022 muddied the water for how business fundamentals actually look. There were a lot of moving pieces and when you have investors moving from one hot theme to the next, there was no reason to own a cheap legacy service company.

Why get in the water now?

Strong / improving fundamental backdrop. While GPN has been seen as a dinosaur losing ground to nimble start ups, the reality on the ground does not bear out those worries. Point of Sale is growing 20% YoY and has done so for the past eight quarters. It re-accelerated in the most recent quarter. Its next gen system launches later this year, providing more opportunities for growth. Meanwhile, GPN’s growth (9% organic) is in line with Visa’s global revenue and nicely above Visa’s US growth. GPN over indexes away from travel, so any switch away from travel and back to consumer goods will be good for GPN.

Competitive threats have proven to not be as powerful as investors feared. BNPL has fizzled. Meanwhile, while GPN doesn’t have the sexy terminal of Clover or Toast, its software and POS work much better for larger restaurants and small chains. That is why it has been able to continue to take share and post strong growth. Its tech enabled share of merchant acquiring is growing high teens or higher and is becoming a greater part of merchant acquiring, which boosts future sales. Further, as VC’s tighten purse strings, former competitors turn into potential acquisitions. GPN has been a savvy acquirer in the past. They recently completed the EVO acquisition and debt has already been paid down by half a turn of EBITDA. I expect we could see new companies, bringing further growth, added to the GPN fold as early as Q1 2024.

New blood. GPN brought in a new CEO on June 1, internally promoting the COO. He is well regarded and I suspect he will continue the playbook that served GPN well over the past two decades while brining in the passion of a new executive.

Technical Breakout: After consolidating for most of the last year, GPN has broken to higher levels. Sell side enthusiasm has also made a marked turn.

Upside Potential

GPN trades at 30x P/E business pre-COVID and the 10 year average P/E is 17x. Given growth and size, 20x seems more than reasonable. The street gives no benefit to acquisitions, buybacks, and new systems for revenue growth, which it slows to mid single digits by 2025. Given GPN has compounded merchant acquiring in the low double digits for years, this is conservative. But allowing for street numbers, EPS comes in ~13.70 in 2025. At 20x, that’s a $275. I am happy to bet on multiple expansion here given the opportunity for higher earnings and the market psychology dynamics at play. This is a 10% position for me. Might be worthwhile to wait to see if it drifts to 116-121 before getting involved or building the position.

Things That Bring Enjoyment

High Art in Video Game Form

I am grateful to my parents who sacrificed so much for my benefit. They raised me in a healthy, happy, stable environment and instilled many lessons that have improved the quality of my life.

BUT… My parents did allow me to play games, which became my guilty pleasure and occasional addition. Maybe because I grew up in a rural area where I didn’t have nearby friends, I gravitated to nerdy RPGs with engaging stories. I still love games with great writing, creative gameplay, or other ways to entertain the player. Because I have more distractions I enjoy in the physical world now than when I was a teen, I try to only play games that are truly amazing and would be considered among the best of all time. These are the games for the thinking set, people of good taste who like shows like Atlanta, What we do in the Shadows, The Wire, or the UK version of The Office. Disco Elysium, Portal, Witcher 3, Last of Us, and the Red Dead Redemption games belong on this list. Baldur’s Gate 3, a recently released masterpiece by Larian Studios, is likely the best computer RPG, and maybe the best game, of all time.

")

Every aspect of this game is exceptional. The writing is incredible, emotional, witty, and engaging. I’ve generally played games aiming for the optimal outcome or to min-max; BG3 makes you embrace random chance going against you and playing the die as they roll. The tactical combat is thought provoking. I never played D&D and I’ve found the systems and UI in games with that inspiration too complicated to deal with; Larian did a great job at simplifying the mechanics to where a new player can take a pre-made character and get going immediately. And… you can hook up with a druid who takes the form of a bear if that’s your thing.